What is DeFi 2.0?

Key takeaways:

- While there is no clear definition of DeFi 2.0, the term generally refers to the projects that build on top of the first generation of DeFi and try to solve the DeFi limitations.

- One of the primary DeFi limitations that DeFi 2.0 tries to overcome is sustainable liquidity provision.

- Some projects have already drawn attention and capital, but the full potential of DeFi 2.0 is yet to be discovered.

Introduction

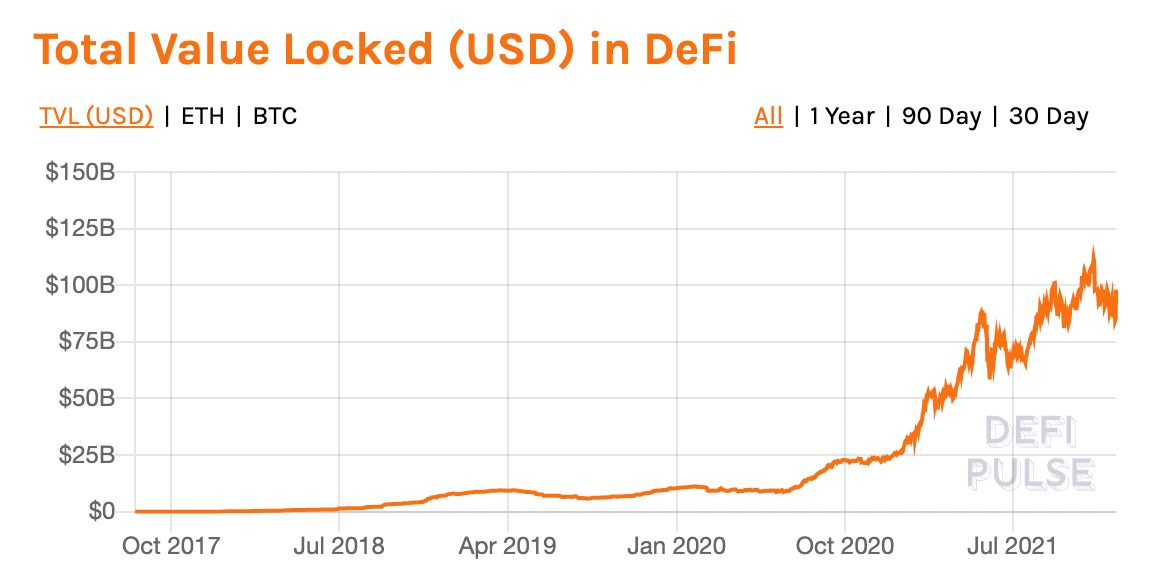

After the “DeFi Summer” of 2020, we have seen further growth in the adoption of DeFi. According to DeFi pulse, the TVL (total value locked) of DeFi reached over $100 billion in November 2021, compared to around $20 billion in September 2020, the unofficial end of 2020 DeFi Summer. After nearly two years of booming, there are currently more than 700 DeFi projects and protocols on the market. In almost every sector of the DeFi, we can see incredibly successful projects like Uniswap, Curve, Aave, Compound, MakerDAO, SushiSwap, etc.

The huge success of DeFi, like what we’ve experienced with BTC and Ethereum, comes with problems too. To solve the problems, a new generation of DeFi projects arises. The term DeFi 2.0 is used to describe new mechanisms that solve the current problems encountered by DeFi projects. In that sense, DeFi 1.0 refers to the first generation of protocols and projects, while DeFi 2.0 builds on top of DeFi 1.0, but is innovative in solving the DeFi 1.0 problems.

Liquidity limitations of DeFi

DeFi projects and protocols are currently facing many problems. Some problems are inherent to blockchain technology, and others are specific to the DeFi innovations. For example, the user experience of DeFi can still not be compared to that of CeFi (Centralized Finance) partly because of the Ethereum scalability problem. DeFi protocols on networks with high traffic and gas often mean slow and expensive services. Another problem DeFi encounters is that it depends on price oracles to get the off-chain data, and this makes oracle the single point of failure for the entire project.

Despite other problems, the most prominent limitation of DeFi is liquidity provision. DeFi democratized the financial market and freed the finance sector from its reliance on regulating bodies, banks, large capital entities, and other intermediaries. The challenge presented by this vision is to ensure enough liquidity to fuel properly functioning markets without intermediaries like banks.

A partial answer to this problem was found in third-party liquidity providers on AMM protocols, through which anyone with funds could provide liquidity. Projects could hypothetically source sufficient liquidity with this method, rather than providing liquidity by themselves. By providing incentives to liquidity providers, this way has proven to be successful in quickly acquiring liquidities. The incentives evolved from yield farming, where LP earns transaction fees, to liquidity mining, where LP receives project tokens as further incentive for providing liquidity.

The problem with that is that LPs are only motivated by the rewards and could leave a protocol if the incentive dries up or if other places provide better incentives. DeFi projects spread across different blockchains and platforms, splitting liquidity. For new projects and projects who haven’t attracted enough liquidity all face a big dilemma: how to bring liquidities in a sustainable way instead of just attracting mercenary capital.

The primary focus of DeFi 2.0 is to revolutionize the common problems associated with liquidity provisioning and incentivization. They provide alternatives and supplements to the yield farming model, giving projects a way to source liquidity that can be sustained for the longer term.

Protocols in DeFi 2.0

There are a few emerging DeFi 2.0 projects which have been trying to solve the liquidity provision problem and other problems, and they are getting the attention of the market. In this article, let’s look at several protocols and learn how they maintain a healthy amount of liquidity, simplify DeFi operations, or increase capital efficiencies.

Olympus DAO

So, we have known that liquidity is a prerequisite for DeFi's continued operation. The liquidity provision mechanism of DeFi 1.0 where liquidity is owned by a third party has exposed problems. Because of that, a new concept called "Protocol Owned Liquidity" was brought up. One of the first implementers of this concept is Olympus DAO.

Olympus DAO is an algorithmic stablecoin protocol that issues and manages fully collateralized, algorithmic, and free-floating stable asset - OHM.

OHM tokens are collateralized by OlympusDAO's Treasury. After the IDO, the tokens are issued to participants at discounted prices in exchange for LP tokens from those who have provided OHM paired liquidity in other platforms. So instead of relying on third-party to provide liquidity, the protocol owns the liquidity.

Protocol Owned Liquidity, also known as Protocol Controlled Value, or PCV, is at the heart of Olympus DAO's innovation. The protocol itself has LP tokens, thus avoiding the short-term bootstrapping problem from liquidity providers, and provides sustainability to the protocol. This changes the relationship between protocols and liquidity providers – in DeFi 1.0, protocols reply on third-party liquidity providers to operate, but for Olympus DAO, the protocol owns most of the token liquidity.

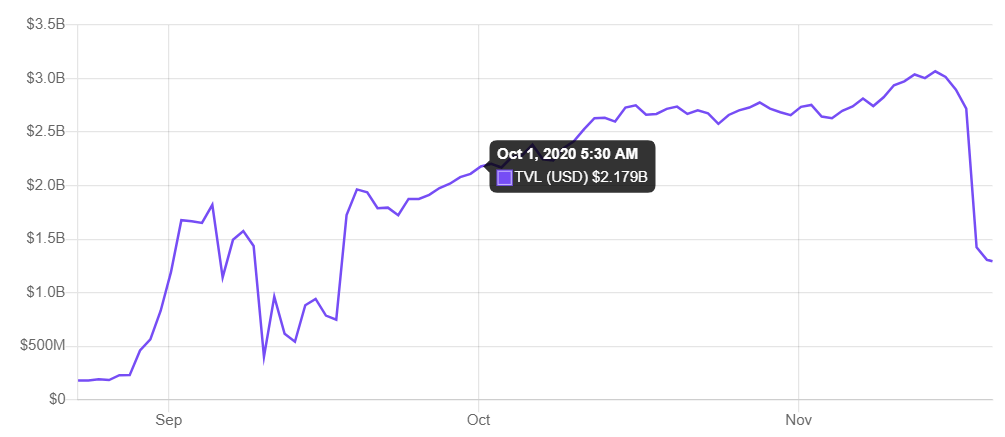

Olympus is trending hard and fast. In under a year, the total value locked (TVL) has grown to $2,382,400,392 as of writing (Dec. 20th, 2021) and is continuing to grow. OHM token price has been riding a rollercoaster, and the (3,3) meme created by the project team is trending beyond the Olympus community.

TokeMak

Tokemak is a decentralized market maker that provides liquidity as a service. What’s innovative about Tokemak is that it tokenizes the liquidity and has a mechanism to direct and influence where liquidity goes.

In first-generation DeFi, liquidity providers are usually required to provide two or more currencies in a certain ratio pre-fixed by the pool at the time of liquidity provision. This causes impermanent loss as the weights shift and the price changes. To combat this, the Tokemak protocol holds reserves of stablecoins and assets that serve as one side of a pair in the liquidity pool. For example, for a Token X-ETH liquidity pool on Uniswap, the Tokemak reserves contribute ETH. Liquidity providers are only required to provide the Token X side of the liquidity. This dramatically reduces the impermanent loss encountered by the liquidity providers.

In Tokemak, each asset has its own pool called a reactor. The more TOKE (Tokemak’s native token) is collateralized in a reactor, the more the protocol directs liquidity to the reactor, meaning the reactor with more collateralized TOKE will attract more liquidity. To guide the liquidity effectively, the protocol introduces the role of liquidity directors. Liquidity directors (LDs), who are the TOKE holders, stake TOKE to guide the liquidity flow, directing liquidity to a wide range of AMM protocols. Liquidity directors receive TOKE as a reward.

The impermanent loss encountered by the liquidity providers are compensated by the reserve, system revenue, staked TOKE, and Protocol Controlled Assets (PCA) in order. In that way, LPs are safeguarded, and both LPs and LDs are incentivized to stay in the protocol.

Convex Finance

Convex is a protocol built on top of Curve Finance. Its sole function is to simply the collateralizing and liquidity mining process on Curve. Instead of going to Curve Finance and taking the multiple steps to do liquidity mining, users can use Convex as a one-stop platform to do liquidity mining with simple clicks.

Here is how it works. Users deposit CRV into Convex to mint token CVX. Then the users will receive rewards from Curve Finance. The rewards include transaction fees and the bonus rewards from Curve. In addition, users will also get CVX, veCRV as rewards. Because of being a liquidity provider on Curve, users will also get a share of the 3crv pool. Unlike in Curve where users are required to lock their assets and are evaluated based on the duration of the LP, Convex users do not need to lock CRV to earn rewards.

In short, Convex simplifies the locking and staking process of CRV on Curve, improves the utility rate of CRV for CRV holders, increases the yield for liquidity providers, and therefore increases the capital efficiency.

Abracadabra

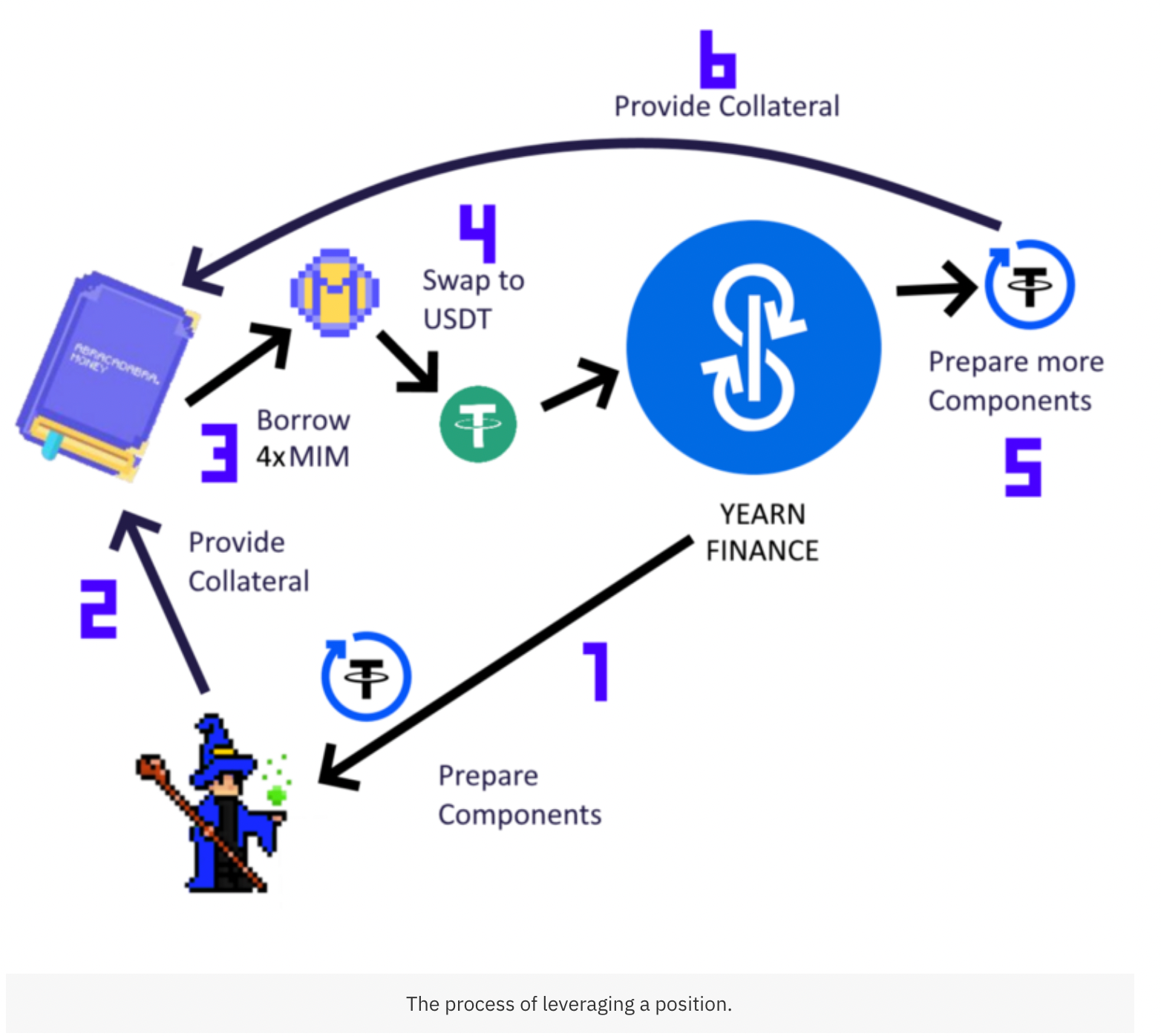

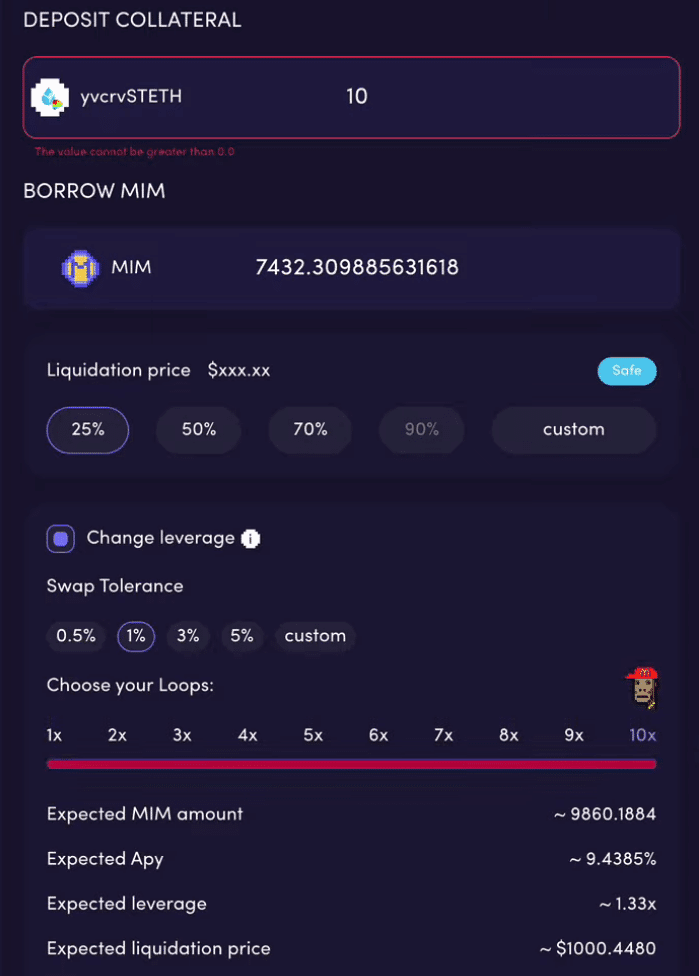

Abracadabra is an asset lending protocol. Similar to MakerDAO, the protocol mints stablecoins MIM (Magic Internet Money) with over-collateralization. What makes Abracadabra special is that it greatly increases capital efficiency, the low of which has been a critic with the first generation of lending protocols.

Unlike the first-generation asset lending agreements, Abracadabra uses interest-bearing assets as collateral. For example, if a user stake USDC on Yearn, the user will receive interest-bearing asset yvUSDC. The user earns rewards from Yearn for holding the yvUSDC but there were not many other applications for this asset. Now with Abracadabra, the user can stake this yvUSDC on Abracadabra, and mint MIM stablecoins. The user can then buy more USDC with MIM, and stake on Yearn again to get more yvUSDC which can then be used to mint more MIM, etc.

Abracadabra allows users to make ten aforementioned cycles in one operation and made the process really easy for users. Interest-bearing assets such as yvYFI, yvUSDT, yvUSDC, yvWETH, and xSushi are all accepted on Abracadabra as collaterals. Users can stake these interest-bearing assets in Abracadabra and mint MIM stablecoins, thereby releasing asset liquidity while at the same time still receiving rewards brought by these interest-bearing assets themselves. This improves the capital efficiency for users. These collateral assets can appreciate in value and the risk of liquidation is reduced.

Closing

DeFi, compared to traditional finance, is still in its early childhood. DeFi 2.0, built on top of the first generation of DeFi, is in its infancy if not earlier. The DeFi 2.0 projects might sound more like a narrative, but the core concepts behind it will most likely stay with us and make liquidity provision more sustainable, capital efficiency higher, trade execution easier and quicker, and application more innovative. While some projects are already successful, the full potential of DeFi 2.0 is yet to be discovered.

Yet, investors should also be aware of the risks when investing in DeFi 2.0 projects. The current DeFi 2.0 is still full of extremely high risks. For example, some people argued that Olympus is essentially a Ponzi’s game and its extremely high APY is not sustainable. Abracadabra is built on top of other projects (yield generating token). If other projects go wrong, then it will also go wrong. Investors should always do their own research when investing in DeFi 2.0.

Discover SynFutures' Crypto Derivatives products: www.synfutures.com/.

Disclaimer: SynFutures Academy does not guarantee the reliability of the site content and shall not be held liable for any errors, omissions, or inaccuracies. The opinions and views expressed in any SynFutures Academy article are solely those of the author(s) and do not reflect the opinions of SynFutures. The SynFutures Academy articles are for educational purposes or information only. SynFutures Academy has no relationship to the projects mentioned in the articles, and there is no endorsement for these projects. The information provided on the site does not constitute an endorsement of any of the products and services discussed or investment, financial, or trading advice. A qualified professional should be consulted prior to making financial decisions.